Closed loops and breaking patterns

N°12 - October 2025

As October closes, this edition explores two divergent paths: systems that circulate capital without creating value, and those that actively transform.

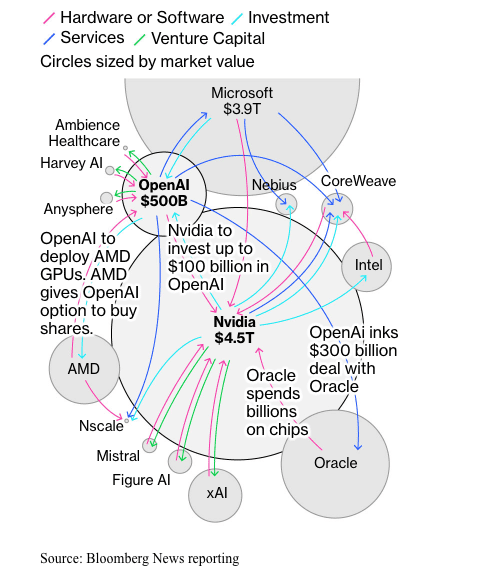

The graph of the week exposes AI’s investment web: Microsoft funds OpenAI, which buys NVIDIA chips, while NVIDIA invests back in OpenAI. Oracle spends billions on the same infrastructure. John Davies argues Apple’s M5 chip positions the company outside this “Ponzi scheme” by delivering on-device performance eliminating data center dependencies.

Dan Milmo’s report on the AWS outage affecting 8.1M users reinforces concentration risks when infrastructure collapses into few providers.

Yet capital is also flowing in new directions. Emily Lai reports 24% of US LPs now increasing European PE exposure, diversifying away from home market concentration. Guillaume Bregeras documents $124 trillion transferring to women by 2048, with female GPs already outperforming by 9.3 percentage points despite managing just 9% of European VC assets, a performance gap that should accelerate change.

Infrastructure shows where investment generates clear returns. The EIC attracted €4B in deeptech co-investment creating tangible results. Ming Yang builds 50-megawatt wind turbines at one-fifth of European costs as China races six years ahead on renewable targets. EIT Urban Mobility shows bike-sharing generating €305M in benefits, a 10% return per euro invested.

Kaushik Basu argues mainstream economics promotes inequality by valorising self-interest over cooperation, a philosophy reinforced by closed systems. Meanwhile, Alexis Akwagyiram notes intra-African trade at just 14% versus 60% for Asia, with sovereignty becoming a priority as protectionism rises.

The contrast is clear: some capital recycles endlessly within established networks, whilst other flows build new systems. The question is which pattern will define the next decade.

We hope this curation will drive your own reflections and actions. Please feel free to share it with those who might be interested.

Let’s dive in! 💫

Insights

Dan Milmo and Graeme Wearden 🇬🇧 report that an AWS outage affecting 2,000+ companies with 8.1M problem reports demonstrates dangerous cloud provider concentration. The Guardian’s analysis shows AWS’s DynamoDB issue from Virginia datacenters prompted experts like Dr Corinne Cath-Speth to call for “urgent diversification in cloud computing” as critical infrastructure including banking and communications remains “at mercy of US tech giants,” whilst UK Parliament questions why Amazon isn’t designated a “critical third party” under financial regulatory oversight despite supporting sector resilience. | The Guardian - CLOUD

John Davies 🇬🇧 argues Apple’s M5 chip positions the company outside the AI infrastructure bubble by delivering on-device performance rivaling cloud solutions at a fraction of the cost. Locally-run open-source models eliminate data center dependencies with zero latency and fixed costs, whilst Apple Silicon outperforms NVIDIA’s $4,000 DGX Spark Desktop, suggesting AI infrastructure spending represents a “Ponzi scheme” where incumbents must maintain trajectory due to sunk costs rather than technical necessity. | LinkedIn - AI

Guillaume Bregeras 🇫🇷 reports that $124 trillion will transfer to women by 2048 with McKinsey projecting two-thirds of US private wealth controlled by women by 2030, reshaping venture capital as female LPs emphasise sustainability and intergenerational well-being. The analysis shows mixed-gender GP teams outperform all-male teams by 9.3 percentage points in median IRR with each 10-point rise in female representation correlating to 1.3-point return increases, yet women manage only 9% of European VC assets while female founders capture just 2% of funding despite generating twice the revenue per dollar invested according to BCG. | 2050 - VC

Emily Lai 🇬🇧 reports that 24% of US LPs plan to increase European PE exposure in 2025 while 12% reduce US allocations due to policy uncertainty and tariffs, offering a “catalytic” lifeline as European fundraising slows with exits restricting distributions. PitchBook analysis shows US capital particularly benefits smaller funds and emerging managers who can now secure anchor investments “almost impossible a couple of years ago,” with larger check sizes complementing European LPs, though US peers’ faster decision-making in co-investment opportunities may challenge European counterparts’ longer governance processes and smaller allocations per deal. | PitchBook - PE

Aisha Malik 🇺🇸 reports Sequoia’s Roelof Botha argued at TechCrunch Disrupt 2025 that venture capital is “return-free risk,” not an asset class, as US VC firms tripled from 1,000 to 3,000 over 20 years while diluting opportunities. Only 380 billion-dollar outcomes emerged in two decades (roughly 20 annually) despite opportunity scale expanding massively from million internet users in 2003 to billions today with mobile and cloud computing, with Botha contending “throwing more money into Silicon Valley doesn’t yield more great companies” but hinders exceptional ones. | TechCrunch - VC

Kirstie Pickering 🇬🇧 reports the European Innovation Council became Europe’s largest deeptech investor, completing 300+ rounds under Horizon Europe (60 in 2024) whilst attracting €4B in co-investment from 600+ VCs and corporates. Sifted’s analysis shows 70 EIC-backed companies reached €100M+ valuations (six exceeding €500M), with portfolio firms averaging 50% increases in employment and turnover within two years, though Hermann Hauser notes Europe produces more startups than the US but only 8% of global scaleups versus 60% in North America, prompting plans for a multi-billion Scaleup Europe Fund targeting early 2026 first close. | Sifted - EIC Investment

Bloomberg News 🇺🇸 reports Ming Yang Smart Energy Group plans a 50-megawatt floating wind turbine, nearly double current largest designs targeting 2026 mass production at under 10,000 yuan ($1,405) per kilowatt versus 50,000 yuan for European offshore turbines. Bloomberg’s analysis shows China’s offshore wind dominance expanding as turbine makers lobby government to more than double installations by decade’s end, whilst Western rivals face high interest rates and material costs, with Ming Yang’s Guangdong facility producing 50 units annually before expanding to 150 as China leads its 2030 renewable targets by six years. | Bloomberg - RENEWABLE ENERGY

Alexis Akwagyiram 🇬🇧 reports AfCFTA Secretary General Wamkele Mene urged accelerating Africa’s free trade area implementation to build resilience against global shocks, citing Washington’s “disregard for trade rules” and AGOA expiration as catalysts for developing domestic markets. Speaking at the FT Africa Summit, Mene noted intra-African trade comprised just 14% of total African trade in 2024 versus 60% intra-regional trade in both Asia and Europe, emphasising supply chain reliability and transport logistics as critical to strengthening economic sovereignty and reducing external dependencies amid rising protectionism. | Semafor - ECONOMIC SOVEREIGNTY

EIT Urban Mobility Study 🇪🇺 reports European bike-sharing schemes generate €305M in annual benefits, avoiding 46,000 tons of CO₂e while preventing 968 chronic diseases and saving €40M in healthcare costs through reduced air pollution. The EY analysis commissioned by EIT Urban Mobility and Cycling Industries Europe shows every euro invested yields 10% annual return (€1.10 in positive externalities) with projections reaching €1B by 2030 if prioritised, supporting 6,000 direct jobs while reclaiming 760,000 congestion hours worth €30M in productivity gains and cutting transport costs up to 90% versus cars. | EIT Urban Mobility - BIKE-SHARING ROI

Kaushik Basu 🇮🇳 argues mainstream economics promotes inequality by treating self-interest as rational and freedom-equality as contradictory, citing Kenneth Arrow’s 1978 paper showing markets depend on trust and cooperation that neoliberal models ignore. Project Syndicate analysis contends economics education encourages selfish behavior while justifying greed, with Arrow noting that when “a few” make “major decisions on which human welfare depends” in their own interests, “formal democracy and freedom” become a “sham” as inequality concentrates power among elites who cynically stoke nationalism to prevent mobilisation against wealth disparities. | Project Syndicate - ECONOMIC

Graph of the week

This edition’s graph from Bloomberg News visualises the circular investment flows between AI’s major players, OpenAI ($500B), Microsoft ($3.9T), NVIDIA ($4.5T), Oracle, and others. Microsoft invests in OpenAI, which buys NVIDIA chips, while NVIDIA invests back in OpenAI. Oracle buys chips whilst partnering with OpenAI. AMD negotiates GPU deals receiving OpenAI equity stakes.

These patterns mirror the 2000 telecom bubble, capital recycling between closed players rather than generating user returns. The network’s density creates concentration risk where one failure could cascade rapidly, amplifying rather than diversifying risk.